.png)

As the Federal Reserve begins cutting rates, financial institutions are reassessing their deposit strategies. While many institutions have relied on rate to drive growth in recent years, evidenced by the surge in CD specials and other high-yield products, the current environment presents new opportunities for attracting and retaining deposits.

The Changing Tides of Deposit Behavior

Historically, rate-cut cycles have been a boon for deposit growth. Total deposits grew during each of the last three easing periods (Source: FRED). This behavior is driven by a simple principle: as interest rates fall, the yield advantage of money market funds, Treasurys, and other products diminishes while banking products become more attractive.

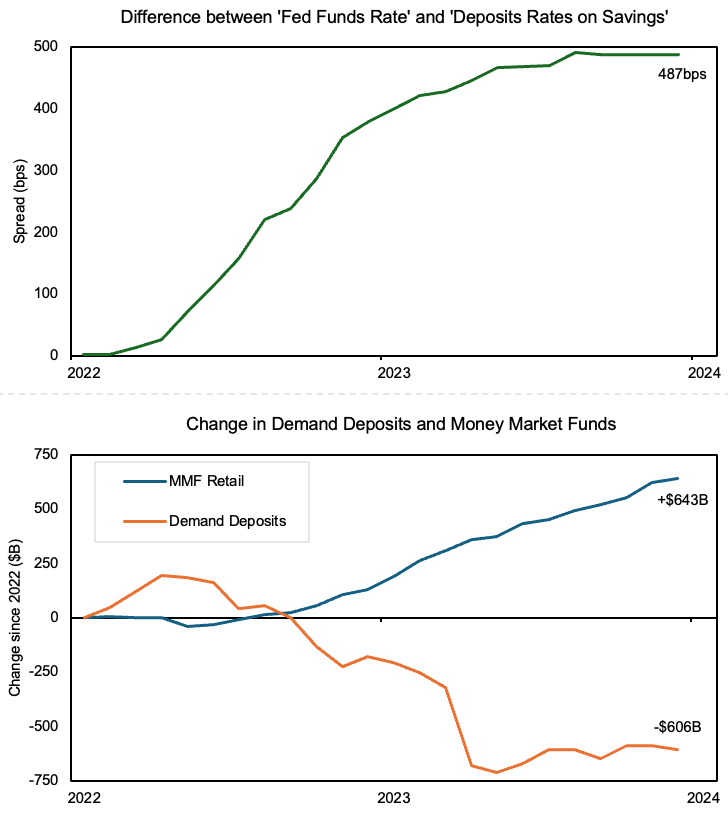

We've observed this relationship play out vividly during the most recent phase of rate hikes. As the difference between the Fed Funds rate versus traditional savings accounts reached its widest point in years, we saw an almost identical flow of funds out of demand deposits ($643B) and into money market funds ($606B), highlighting the sensitivity of deposits to rate changes.

The New Deposit Paradigm

However, as we enter a rate-cut cycle, the playbook for deposit growth is being rewritten:

- Shift to Liquidity: As interest rates decrease, expect a migration from term deposits to more liquid savings and checking accounts as the yield advantage of locking up money diminishes.

- End of CD Gold Rush: The era of high-yield CD specials is drawing to a close. Institutions that relied heavily on rate-driven strategies will need to pivot to retain maturing deposits.

- Deposit Stability: Interestingly, these deposits flowing back into the market may be stickier. Lower rates reduce the attractiveness of products like money market funds, leading to more stable demand deposits as rate-seeking opportunities dry up.

Non-rate Deposit Growth Levers in the New Normal

As rate becomes a less effective lever for growth, deposit networks offer powerful use cases for institutions to adapt and thrive:

- Security as a Differentiator: With rate advantages diminishing, security becomes a stronger differentiator. Institutions can now compete for high-value deposits by offering accounts with extended deposit insurance* that highlight enhanced protection for security-conscious individuals, businesses, and public entities.

- Precision Balance Sheet Management: The ability to sweep excess deposits off-balance sheet through the network gives institutions precise control over their balance sheet size and composition – crucial in an environment where deposit growth may outpace loan demand.

- Diversifying Funding Sources: By tapping into a broader pool of depositors through extended insurance accounts, institutions can reduce concentration risk and build a more resilient funding base. This includes attracting deposits from businesses, municipalities, and nonprofits that may have previously been out of reach.

At ModernFi, we're dedicated to equipping financial institutions with the tools and technology needed to succeed in this new environment. As we navigate this transition, financial institutions have a unique opportunity to reimagine their strategies as depositors shift away from money market funds. By focusing on non-rate value propositions like extended insurance and harnessing the power of deposit networks, financial institutions can build a more resilient, diversified funding base that will thrive across rate environments.

Best,

The ModernFi Team

* Deposit insurance provided by program institutions (subject to meeting certain conditions)

Sources: Deposit and rate data provided by FRED

Disclosures:

The market, service, or other information is provided solely for your information and “AS IS” and “AS AVAILABLE”, without any representation or warranty as to accuracy, adequacy, completeness, timeliness, or fitness for particular purpose. The user bears full responsibility for all use of such information. ModernFi may provide updates as further information becomes publicly available but will not be responsible for doing so. The terms, conditions, and descriptions that appear are subject to change; provided, however, ModernFi has no responsibility for updating or correcting any information provided in this communication. No member of the ModernFi organization shall have any liability to any person receiving this communication for the quality, accuracy, timeliness, or availability of any information contained in this communication or for any person’s use of or reliance on any of the information, including any loss to such person.

All information contained herein is for informational purposes and should not be construed as investment advice. It does not constitute an offer, solicitation, or recommendation to purchase any security, and is not intended to provide, and should not be relied on for, tax, legal, or accounting advice. The information contained herein is for institutional use only.

Neither ModernFi Deposit Services LLC, ModernFi CUSO LLC, ModernFi Inc. (collectively ModernFi) nor any of its affiliates are a bank, nor do they offer bank deposits and their services are not guaranteed or insured by the FDIC or NCUA. ModernFi’s deposit network is not a member of the Federal Deposit Insurance Corporation (FDIC) or National Credit Union Administration (NCUA), but the banks where money is deposited are FfDIC members and the credit unions where money is deposited are NCUA members. The maximum FDIC or NCUA insurance per Tax ID at each institution is $250,000. If customers have additional deposits at any depository institution that is in ModernFi’s network, then they may not receive full FDIC or NCUA-insurance coverage on the deposits at those institutions. The FDIC is an independent agency of the U.S. government that protects the funds depositors place in FDIC-insured institutions. The NCUA is an independent agency of the U.S. government that protects the funds depositors place in NCUA-insured institutions. FDIC and NCUA deposit insurance is backed by the full faith and credit of the U.S. government.

Any rates shown are hypothetical only and current rates / maximum deposit insurance coverage are subject to change at any time due to changes in market or business conditions. Past performance does not guarantee future results.

All trademarks, logos and brand names are the property of their respective owners. All company, product, and service names used in this website are for identification purposes only. Use of these names, trademarks, and brands does not imply endorsement.

Unauthorized use of the provided information or misuse of any information is strictly prohibited.

ModernFi's deposit network is offered by ModernFi Deposit Services LLC, a wholly-owned subsidiary of ModernFi, Inc.

© 2024 ModernFi, Inc. All rights reserved.