.png)

Insights

Thought Leadership

Momentum Around Deposit Insurance Reform Dissipates in Congress

July 25, 2023

The Senate Banking Committee met last week to discuss deposit insurance reform in the wake of the bank failures earlier this year, and the results were underwhelming. Despite repeated calls from the banking sector for increases to deposit insurance limits, either across the board or for specific categories of depositors, lawmakers seem to have little appetite for change.

Committee Chair Sherrod Brown, D-Ohio, was clear that he is not convinced “what changes, if any, should be made”, and Senator Mark Warner, D-Va., summed up the hearings with, “It feels to me like a lot of the energy around the FDIC in terms of reform has kind of dissipated a little bit.”

The change in momentum is disappointing for many in the industry, given how much urgency the topic had earlier this year and given how helpful reform would be for smaller banks across the country. Small and midsize banks have seen large amounts of uninsured deposit outflows as large-value depositors worried about the security of their funds have left for larger institutions and money markets.

The ability to offer higher insurance would help smaller banks attract and retain large depositors and help them grow in an increasingly competitive banking landscape, while also reducing run risk in the sector. The lack of action from Congress, despite repeated calls for help, will force banks to take their destiny and their fate into their own hands.

We’ve been vocal that we believe reciprocal and sweep products, which provide extended insurance to depositors by allocating deposits into a network of receiving banks, provide a beautiful solution. Banks can make their depositors eligible for extended insurance, without losing deposits in aggregate and without losing their customer relationships. Reciprocal products have become essential to banks’ operating model, and we, as many of you know, are hard at work making sure the products are enjoyable for both banks and their depositors.

Best,

Paolo and the ModernFi Team

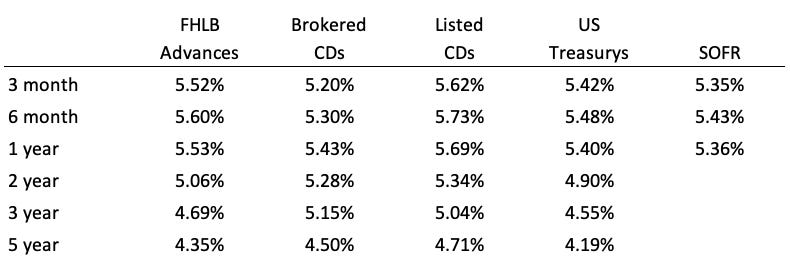

Current rates

Change from two week ago

Sources: FHLB Advances are an average of FHLB Boston, FHLB Chicago, and FHLB Des Moines. Brokered CDs are an average of Fidelity and Vanguard. Listed CDs provided by National CD Rateline. US Treasurys provided by WSJ. SOFR provided by CME.

Please feel free to share this post from ModernFi Insights with those that might be interested. Thanks!

Disclosures:

All information contained herein is for informational purposes and should not be construed as investment advice. It does not constitute an offer, solicitation or recommendation to purchase any security, and is not intended to provide, and should not be relied on for, tax, legal or accounting advice. Past performance does not guarantee future results. The information contained herein is for institutional use only.

ModernFi Advisers LLC (ModernFi) is not a bank, nor does it offer bank deposits and its services are not guaranteed or insured by the FDIC; ModernFi allocates funds to banks that are FDIC members.

Certain information contained herein has been obtained from third party sources and such information has not been independently verified by ModernFi. No representation, warranty, or undertaking, expressed or implied, is given to the accuracy or completeness of such information by ModernFi or any other person. While such sources are believed to be reliable, ModernFi does not assume any responsibility for the accuracy or completeness of such information. ModernFi does not undertake any obligation to update the information contained herein as of any future date.

Certain information contained herein constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance or a representation as to the future.

Except where otherwise indicated, the information contained in this communication is based on matters as they exist as of the date of preparation of such material and not as of the date of distribution or any future date. Recipients should not rely on this material in making any future investment decision.