.png)

2023 was a transformative year for banking. Continued rate hikes from the Fed, coupled with the banking stress in March, led to a dramatic change in funding composition across U.S. banks. Core deposits ran off from the system looking for yield and stability elsewhere, and institutions turned to wholesale funding markets to replace runoff and smooth lending. Moving into this new year, we expect these trends to stabilize and moderate, but we expect to see continued heavy usage of wholesale funds and increased competition for core deposits, especially for the largest-value depositors.

Examining changes in aggregate funding over the past two years makes these trends clear. Since the start of 2022, uninsured core deposits ran off extremely quickly, falling by $1.8 tn, as large-value depositors left looking for higher yields (prompted by rising rates) and security (prompted by the banking turmoil). The runoff in uninsured core deposits was so large that it countered growth in other funding sources, leading to total deposits falling by $1.2 tn across the industry. Insured core deposits remained flat; in more normal periods, we would expect to see consistent ~5% annual growth there.

On the wholesale side, we saw significant growth in brokered deposits, growing by $693 bn over the 2-year period. FHLB usage also increased by roughly the same amount before falling slightly. We assume that, starting in Q1 2023, some FHLB Advances were replaced with Bank Term Funding Program (BTFP) funds, leading to the slight decline in FHLB and the rise in Borrowed Funds, which includes BTFP.

Looking ahead, we expect these trends to continue, albeit less aggressively. The Fed raised rates by 4.25% in 2022 and 1.00% in 2023. Over 2024, despite opinions from pundits and press, we expect the Fed to remain conservative and keep rates steady for as long as possible. We would only expect rates to be cut if the economy significantly declines. (Our funding expectations for 2023 were more or less correct, which has overinflated our self-confidence when it comes to predicting unpredictable things.)

As institutions move into this new year, we recommend focusing on the largest-value depositors to stem runoff, and continuing to keep wholesale funding lines open to smooth the edges. All in all, we’re hopeful for a good year with less stress and a healthy return to banking normalcy.

Best,

The ModernFi Team

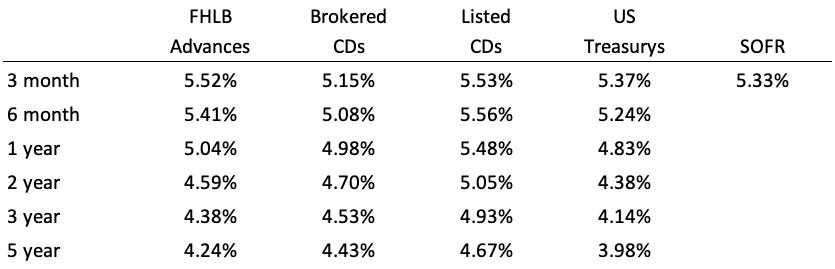

Current rates

Change from five weeks ago

Sources: FHLB Advances are an average of FHLB Boston, FHLB Chicago, and FHLB Des Moines. Brokered CDs are an average of Fidelity and Vanguard. Listed CDs provided by National CD Rateline. US Treasurys provided by WSJ. SOFR provided by Chatham Financial.

Funding data aggregated by ModernFi from FFIEC Call Reports as of 9/30/23.

Disclosures:

All information contained herein is for informational purposes and should not be construed as investment advice. It does not constitute an offer, solicitation or recommendation to purchase any security, and is not intended to provide, and should not be relied on for, tax, legal or accounting advice. Past performance does not guarantee future results. The information contained herein is for institutional use only.

ModernFi Advisers LLC (ModernFi) is not a bank, nor does it offer bank deposits and its services are not guaranteed or insured by the FDIC; ModernFi allocates funds to banks that are FDIC members.

Certain information contained herein has been obtained from third party sources and such information has not been independently verified by ModernFi. No representation, warranty, or undertaking, expressed or implied, is given to the accuracy or completeness of such information by ModernFi or any other person. While such sources are believed to be reliable, ModernFi does not assume any responsibility for the accuracy or completeness of such information. ModernFi does not undertake any obligation to update the information contained herein as of any future date.

Certain information contained herein constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance or a representation as to the future.

Except where otherwise indicated, the information contained in this communication is based on matters as they exist as of the date of preparation of such material and not as of the date of distribution or any future date. Recipients should not rely on this material in making any future investment decision.