.png)

2022 marked a regime change in funding markets. Other than a modest increase in interest rates from 2015-2018, the Fed had kept short-term rates near zero since 2008. In addition, fiscal and monetary stimulus during the COVID pandemic led to an abundance of deposits and liquidity in the financial sector. At the end of Q1 2022, much of that changed when the Fed began aggressively raising rates to counter inflation. Rising rates has led to a sharp decrease in bank deposits as funds have moved to other asset classes. Given the Fed’s steadfast stance on inflation, we expect rates to continue rising this year, and we expect funding to become more of a concern for banks.

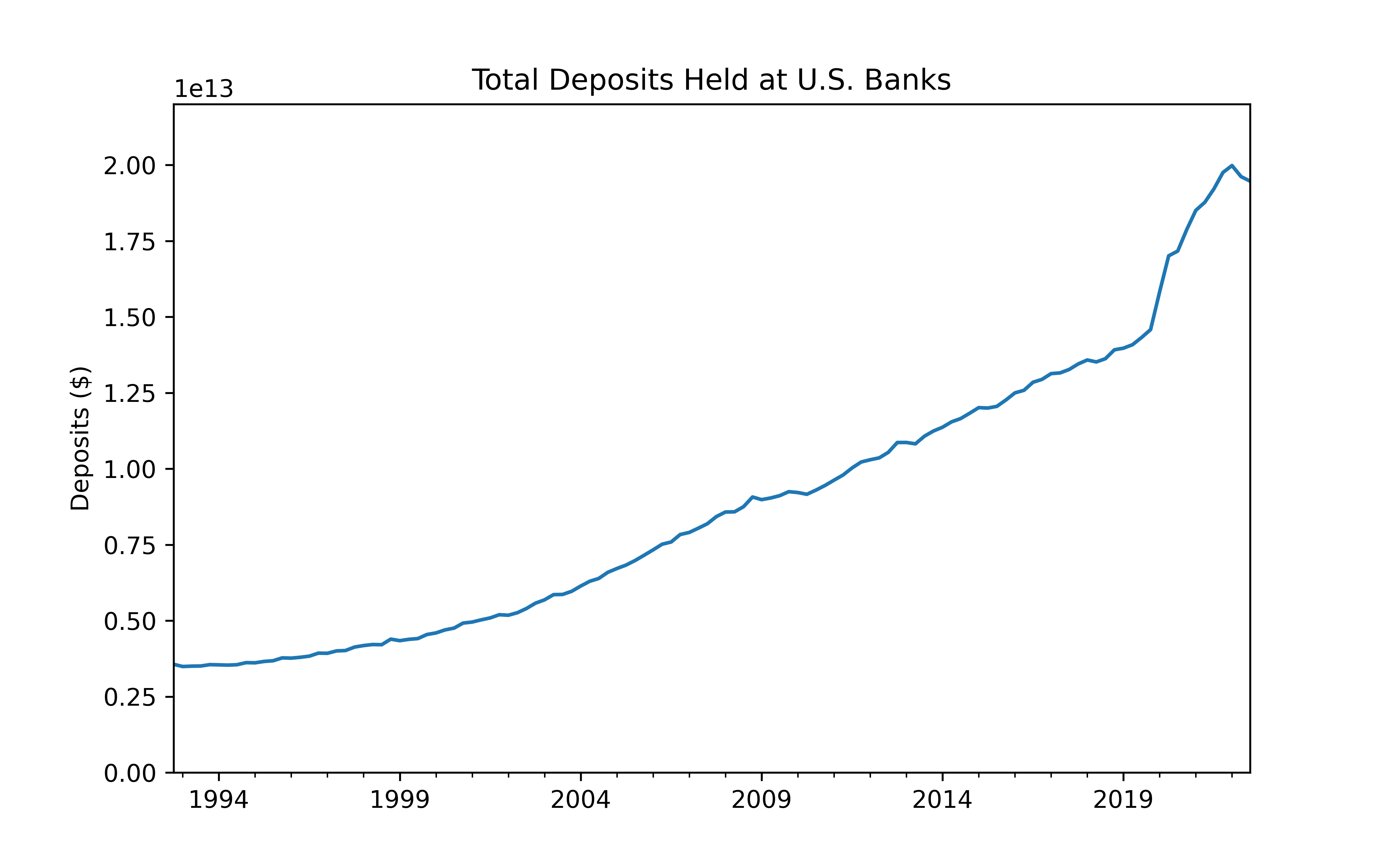

From Q1 2022 through Q3 2022, the Fed raised Interest on Reserve Balances (IORB), the rate that banks earn from depositing money at the Fed, from 0.15% to 3.15%. Total deposits at depository institutions fell $514.10 billion from $19.98 trillion to $19.47 trillion over the period. The 2.6% decline is the largest 6-month decrease in deposits, both in absolute and percentage terms, since the FDIC started publishing data in 1992. However, overall deposits in the system remain well above pre-pandemic levels (total deposits stood at $14.58 trillion at the end of 2019; see figure below).

Despite high deposit levels relative to history, sourcing funding has become a major focus for depository institutions. From Q1 through Q3 2022, the amount of wholesale funding purchased by banks increased by $562.54 billion from $4.37 trillion to $4.94 trillion, as banks tapped wholesale funds to offset the decline in deposits, manage liquidity, and maintain asset origination.

We expect deposits to continue draining from the system throughout the year. The Fed is expected to continue raising rates through 2023 (Fed officials currently expect the end-of-year rate to be ~5.25%), and we do not expect rate stabilization or rate cuts in the near future. History has shown that loosening monetary policy too soon has worse long-term effects than staying hawkish for too long, and Chairman Powell and the FOMC are no doubt well aware of this history.

Rising rates has led to a new regime in funding availability, and banks with access to a range of funding sources will be best situated for the coming years.

Best,

Paolo and the ModernFi Team

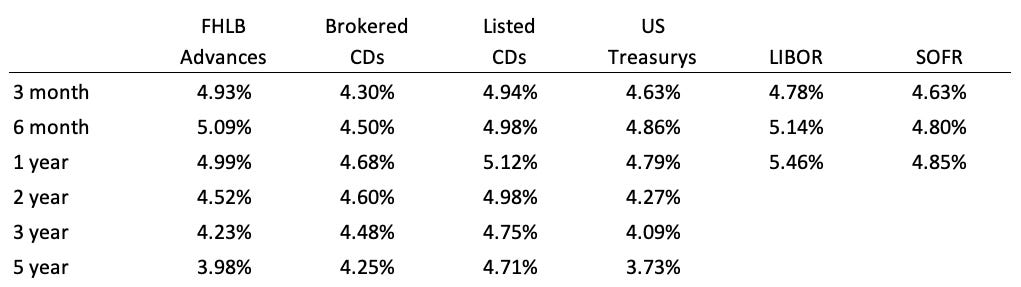

Current rates

Change from four weeks ago

Sources: FHLB Advances are an average of FHLB Boston, FHLB Chicago, and FHLB Des Moines. Brokered CDs are an average of Fidelity and Vanguard. Listed CDs provided by National CD Rateline. US Treasurys and LIBOR provided by WSJ. SOFR provided by CME.

Data on deposits and wholesale funding is sourced from the FDIC’s BankFind Suite API. The figure uses quarterly data.

Please feel free to share this post from the Wholesale Funding Update with those that might be interested. Thanks!

Disclosures:

All information contained herein is for informational purposes and should not be construed as investment advice. It does not constitute an offer, solicitation or recommendation to purchase any security, and is not intended to provide, and should not be relied on for, tax, legal or accounting advice. Past performance does not guarantee future results. The information contained herein is for institutional use only.

ModernFi Advisers LLC (ModernFi) is not a bank, nor does it offer bank deposits and its services are not guaranteed or insured by the FDIC; ModernFi allocates funds to banks that are FDIC members. ModernFi is an investment adviser registered with the United States Securities and Exchange Commission (SEC). For more information regarding the firm, please see its Form ADV on file with the SEC through the Investment Adviser Public Disclosure website. Registration with the SEC does not imply a particular level of skill or training.

Certain information contained herein has been obtained from third party sources and such information has not been independently verified by ModernFi. No representation, warranty, or undertaking, expressed or implied, is given to the accuracy or completeness of such information by ModernFi or any other person. While such sources are believed to be reliable, ModernFi does not assume any responsibility for the accuracy or completeness of such information. ModernFi does not undertake any obligation to update the information contained herein as of any future date.

Certain information contained herein constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance or a representation as to the future.

Except where otherwise indicated, the information contained in this communication is based on matters as they exist as of the date of preparation of such material and not as of the date of distribution or any future date. Recipients should not rely on this material in making any future investment decision.