.png)

We’ve written at length about the large amount of deposits that have runoff from the banking sector over the previous quarters. As interest rates have risen, depositors have pulled funds from banks and reinvested in higher-yielding asset classes. The yields on other assets such as Treasurys, municipal bonds, and commercial paper tend to rise more quickly than the yields on bank accounts. Money market funds (MMFs), which provide investors with an easy way to invest in the aforementioned assets, have seen huge inflows in recent months [1].

Assets in money market funds have reached record levels. The funds held $5.18 trillion at the end of December 2022, and an additional $135 billion flowed into the funds in January alone [2]. The yield differential compared to bank accounts is stark, with U.S. funds yielding above 4% on average while the average savings account yields 0.35% [3].

Importantly, the runoff to money funds disproportionately affects smaller banks. Large, complex institutions are active in a variety of funding markets and issue commercial paper, which is then purchased by money funds, returning some of the runoff right back to the institutions. Smaller institutions, including most community banks, don’t have access to and don’t participate in these markets. They don’t issue paper and don’t receive any investment from money funds.

The asymmetric return of deposit runoff across the banking sector highlights the need for more accessible, transparent, and efficient funding markets open to all banks [4].

Best,

Paolo and the ModernFi Team

Notes and Sources

Credit for this asymmetric return idea goes to our academic friends at Harvard

[1] As a historical tangent, MMFs were created because investors needed a place to hold short-term cash, and regulation (Reg Q from the Fed) prohibited demand deposit accounts from paying interest and limited the amount of interest that banks could pay on other account types. If the regulation had been different, MMFs may never have caught on, and these deposits might still be at banks today…

[2] Data on asset totals from EPFR and data on flows from Crane (both behind paywall)

[3] Data on MMF yields from Crane and bank account yields from FDIC

[4] We’re obviously a little biased over here at ModernFi

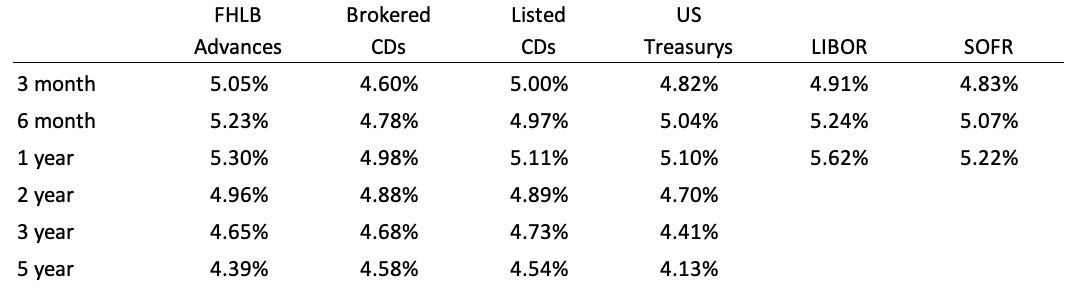

Current rates

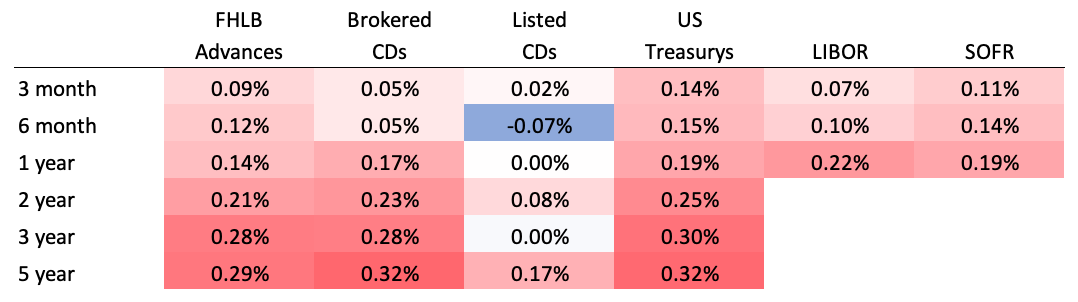

Change from two weeks ago

Sources: FHLB Advances are an average of FHLB Boston, FHLB Chicago, and FHLB Des Moines. Brokered CDs are an average of Fidelity and Vanguard. Listed CDs provided by National CD Rateline. US Treasurys and LIBOR provided by WSJ. SOFR provided by CME.

Please feel free to share this post from the Wholesale Funding Update with those that might be interested. Thanks!

Disclosures:

All information contained herein is for informational purposes and should not be construed as investment advice. It does not constitute an offer, solicitation or recommendation to purchase any security, and is not intended to provide, and should not be relied on for, tax, legal or accounting advice. Past performance does not guarantee future results. The information contained herein is for institutional use only.

ModernFi Advisers LLC (ModernFi) is not a bank, nor does it offer bank deposits and its services are not guaranteed or insured by the FDIC; ModernFi allocates funds to banks that are FDIC members. ModernFi is an investment adviser registered with the United States Securities and Exchange Commission (SEC). For more information regarding the firm, please see its Form ADV on file with the SEC through the Investment Adviser Public Disclosure website. Registration with the SEC does not imply a particular level of skill or training.

Certain information contained herein has been obtained from third party sources and such information has not been independently verified by ModernFi. No representation, warranty, or undertaking, expressed or implied, is given to the accuracy or completeness of such information by ModernFi or any other person. While such sources are believed to be reliable, ModernFi does not assume any responsibility for the accuracy or completeness of such information. ModernFi does not undertake any obligation to update the information contained herein as of any future date.

Certain information contained herein constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance or a representation as to the future.

Except where otherwise indicated, the information contained in this communication is based on matters as they exist as of the date of preparation of such material and not as of the date of distribution or any future date. Recipients should not rely on this material in making any future investment decision.